Finance

Finance

Prudhoe Town Council as a public body is responsible for its own finances. It is required to make arrangements for the proper administration of its financial affairs and to ensure that one of its officers has this responsibility. The officer whose job it is to oversee the finances of the Council is referred to as the Responsible Financial Officer (RFO).

The Council must work within a legal framework that is specified within the Accounts and Audit Regulations and it must ensure that its business is conducted in accordance with the law and proper standards.

Good governance, accountability and transparency are essential and a cornerstone to improving public services. The Council must ensure that public money is safeguarded, properly accounted for and used economically, efficiently and effectively.

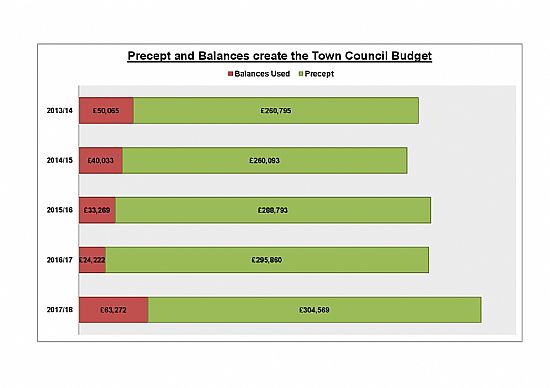

The Town Council begins the process of setting its budget in November, a draft is presented to a January budget meeting and at this time the budget is set and the precept demand agreed.

You can compare the Budget set and the Precept demand over the last 5 years below; please click on the chart to view in a larger PDF format:

The precept demand is the money collected by Northumberland County Council, from the council tax payers of Prudhoe, on behalf of Prudhoe Town Council. The Town Council receives this money in 2 installments over the financial year.

The Town Council pays for services and responsibilities through their budget. This is made up, in the main, from the precept (as described above), in addition to income from sponsorship and events, burial fees, the reclaim of VAT, grants and any balances from the previous year.

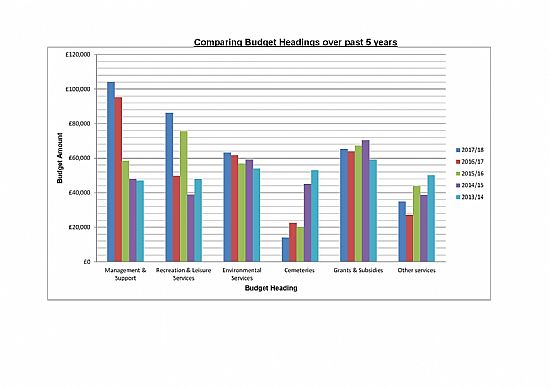

You can compare Budget Headings over the last 5 years below; please click on the chart to view in a larger PDF format:

As well as budgeted spending, the council does hold money in a contingency heading, to cope in the event of the unknown. Additionally, it is the council’s aim to increase its Asset Reserve Fund in order to ensure its assets are properly maintained and developed in the future.

Local Councils have few Statutory Duties but many Specific Powers. Statutory Duties set out what a council MUST do, mostly as a result of having the power to raise a precept or more specific legislative requirements as a public body.

Legislation permits, but does not impose, a greater range of specific powers and allows local councils the freedom to choose the discretionary services they wish to exercise. Prudhoe Town Council has exercised its discretionary powers to provide, manage and maintain:

Public Toilets (Public Health Act 1936, s87)

Edgewell Cemetery (Local Government Act 1972, s214)

Bus Shelters (Local Government (Misc. Provisions) Act 1953, s4)

Litter Bins (Litter Act 1983, ss5-6)

The Town Council does not have a statutory duty to carry out many of the activities it does in its Budget (other than the ‘duty’ to provide allotments), however the Town Council does have the ‘power’ to spend money as detailed in the ‘Powers and Duties’ list decreed by Government.

Every item of expenditure authorsied by the council has to be supported by a statutory power of expenditure. Each month a payment schedule is produced and presented to the Ordinary Meeting which details the relevant power. The payment schedule for each month is available to view in the table for each financial year.

The Audit Commission continually monitor the performance of the external auditors, assessing the quality of their work and ensuring they carry it out in compliance with their statutory obligations. The Smaller Authorities Audit Appointments Limited (SAAA) have appointed Mazars as our external auditors for 2022/23. They can be contacted at:

Smaller Authorities External Audit Team, Mazars LLP

0191 3836348

local.councils@mazars.co.uk

Prudhoe Town Council is also required to appoint an Internal Auditor who will monitor and review the arrangements in place to ensure the proper conduct and effectiveness of our financial affairs. Our internal auditor is Mrs Susan Saunders.

The Council must have an adequate system of internal control and risk management. This review is an integral part of continually improving governance and accountability. The Council is required to publicly report the outcome of the review of its accounts and to make its accounting statements and other documents available for public inspection. The results of the External Audit are available to view on the website and on request, this is in the form of an Annual Return, different to the tax return that is completed by most organisations. The Annual Return is completed in June and usually returned in September, five months after the end of the financial year. During this period, members of the public are invited to look at the council’s accounts, however, residents may at any time ask to see the council’s accounts and questions relating to spending can always be put to the Town Clerk/RFO.

If you have any questions about the financial governance of the council, our budget or specific spending, throughout the year, please feel free to contact us.

Click on the link to view the Annual Audit Process.